How to Calculate Your Debt-Free Date (and Pay Off Debt Faster)

Ask anyone paying off debt what they want most and the answer is rarely a dollar figure - it's a date. The day the last payment clears and the balances read zero. That day has a name: your debt-free date. And unlike most financial goals, it can be calculated precisely from numbers you already have.

This guide explains exactly how a debt-free date is computed, why the order you pay debts in changes that date, and the specific levers that pull it closer.

What a debt-free date actually is

Your debt-free date is the month every one of your debts reaches a zero balance, given three things:

- The balance and interest rate of each debt.

- The minimum payment required on each.

- Any extra payment you can throw at debt beyond the minimums.

Each month, interest is added to every balance, your payments are subtracted, and the balances shrink. The debt-free date is simply the month that process finishes. The interesting part is what happens to your extra payment - because how you direct it can change the date by years.

The month-by-month math

For a single debt, each month follows the same loop:

- Add one month of interest: balance × (annual rate ÷ 12).

- Subtract your payment.

- Carry the new balance to next month - repeat until it hits zero.

A $5,000 credit card at 22% APR with a $150 payment accrues about $92 of interest the first month, so only ~$58 actually reduces the balance. That's why high-interest debt feels like wading through mud - most of your payment is feeding the interest, not the principal.

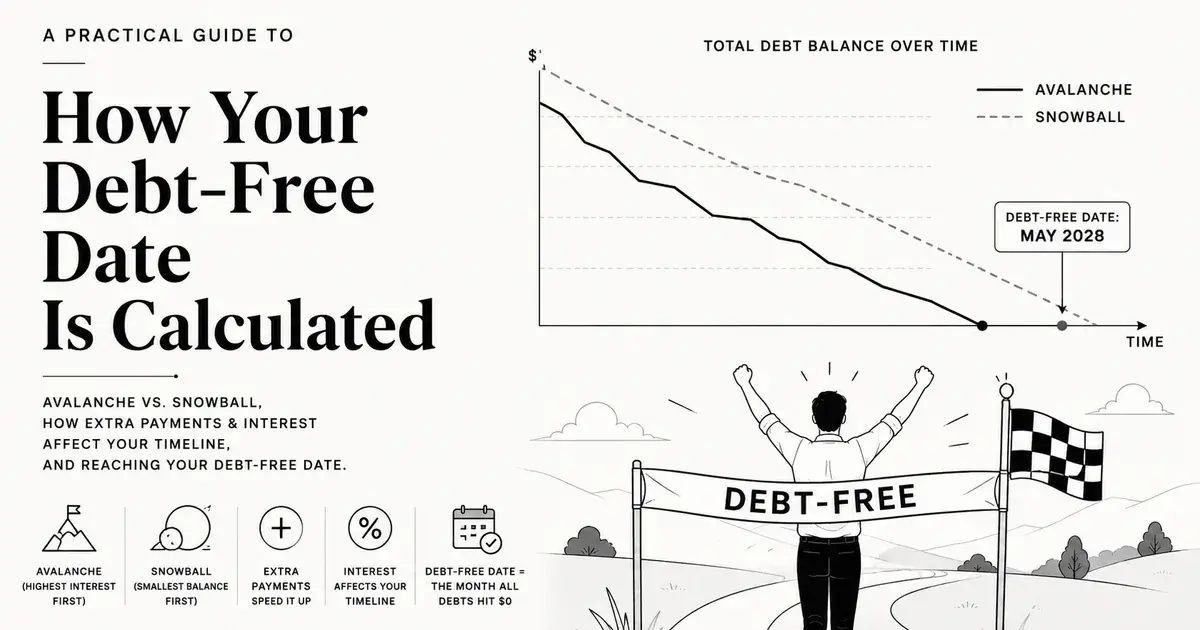

Avalanche vs. snowball

With multiple debts, you pay every minimum, then send your extra payment to one target debt. The two popular strategies disagree on which debt that should be.

The avalanche method (lowest total interest)

Target the debt with the highest interest rate first. Once it's gone, roll its entire payment onto the next-highest rate, and so on. Because you're always killing your most expensive debt, the avalanche method mathematically minimizes the total interest you pay and produces the earliest possible debt-free date for a given budget.

The snowball method (fastest psychological wins)

Target the smallest balance first, regardless of rate. You clear individual debts faster, which feels motivating - but you may pay more interest overall and reach your final debt-free date later than the avalanche would.

Both retire your debt. Avalanche optimizes the dollars; snowball optimizes the momentum. If you trust yourself to stay the course, the avalanche wins on every objective metric.

A worked example

Imagine three debts and $1,200/month total to spend on them:

- Credit card: $6,000 at 22% APR, $120 minimum.

- Car loan: $12,000 at 7% APR, $300 minimum.

- Student loan: $9,000 at 5% APR, $150 minimum.

Minimums total $570, leaving $630 extra each month. The avalanche method sends all $630 to the 22% credit card first. Once it clears, that whole $750 (its minimum plus the extra) cascades onto the car loan, then later the combined payment hits the student loan. Each payoff accelerates the next - the snowball effect, applied in the most interest-efficient order. Compared with paying only minimums, this can pull the debt-free date forward by years and save thousands in interest.

The bars above tell the whole story: snowball and avalanche both crush the “minimums only” baseline, and the avalanche edges out the snowball on both time and interest because it always attacks the most expensive debt first.

The levers that move your date earlier

- Increase the extra payment. Even $100 more a month compounds across every debt in the cascade.

- Attack the highest rate first. Switching from snowball to avalanche order is free and only moves the date earlier.

- Lower a rate. Refinancing or a balance transfer means more of each payment hits principal.

- Apply windfalls. A tax refund or bonus dropped onto the top-priority debt can erase months at once.

Calculating it in FinProjection

Doing this loop by hand across several debts is tedious and error-prone. FinProjection runs the full month-by-month calculation for you: enter each debt's balance, rate, and minimum payment, and it applies the avalanche strategy automatically - paying the highest-rate debt first and cascading freed-up payments onto the next.

It then shows your exact debt-free date and lets you test the levers above in real time: nudge the extra payment up and watch the date jump earlier. Because debt payoff feeds directly into your broader long-term financial projection, you also see how clearing your debts frees up cash flow to build net worth in the years that follow.

It's free, needs no signup, and runs entirely in your browser - so your debt details never leave your device.

See your own numbers

FinProjection turns your real income, expenses, debts, and assets into a clear 10-year roadmap - with growth, inflation, and the avalanche debt strategy built in. Free, no signup, 100% in your browser.

Try It Now - It's Free

FinProjection is a planning tool, not financial advice. Projections are estimates based on the assumptions you enter and are not guarantees of future results. Consult a qualified financial professional before making major financial decisions.