How to Build a Long-Term Financial Projection for Your Family

Most families track spending with a monthly budget. A budget answers “Did we overspend this month?” - but it can't answer the questions that actually keep you up at night: Can we afford a second child? When could we put a down payment on a house? Will we be okay if one income disappears for a year? Those are projection questions, and they need a longer lens.

A long-term financial projection turns today's income, expenses, debts, and savings into a month-by-month forecast of your net worth over the next 5 to 10 years. This guide walks through how to build one for your family - the inputs that matter, the assumptions to get right, and the common mistakes that make projections useless.

Budget vs. projection: why the long lens matters

A budget is a snapshot; a projection is a trajectory. The difference compounds - literally. A family saving an extra $400 a month at a 6% return doesn't just have $4,800 more after a year. After ten years they have roughly $65,000 more, because returns earn returns. You can't see that in a monthly budget. You can only see it when you project forward.

The four inputs every family projection needs

A credible projection rests on four building blocks. Get these roughly right and the output is useful; guess wildly and it's fiction.

1. Income (and how it grows)

Start with every income source: salaries, a partner's freelance work, rental income, side gigs. The key move that separates a real projection from a spreadsheet of today's numbers is growth. Salaries typically rise 2–4% a year with raises and promotions. If you assume your income is frozen for a decade, your projection will badly understate where you'll be.

2. Expenses (and inflation)

List recurring expenses - housing, food, childcare, transport, insurance - plus the irregular ones families forget: car replacement, home repairs, annual travel. Then apply an inflation rate (3% is a reasonable default) so a $1,500 grocery bill today is modeled correctly as a larger number in year eight.

3. Assets (and compounding returns)

Include savings accounts, retirement accounts, brokerage investments, and home equity. Each can grow at its own rate - a high-yield savings account at 4%, a stock portfolio at a long-run 6–7%. This is where most of your net worth growth comes from over a decade.

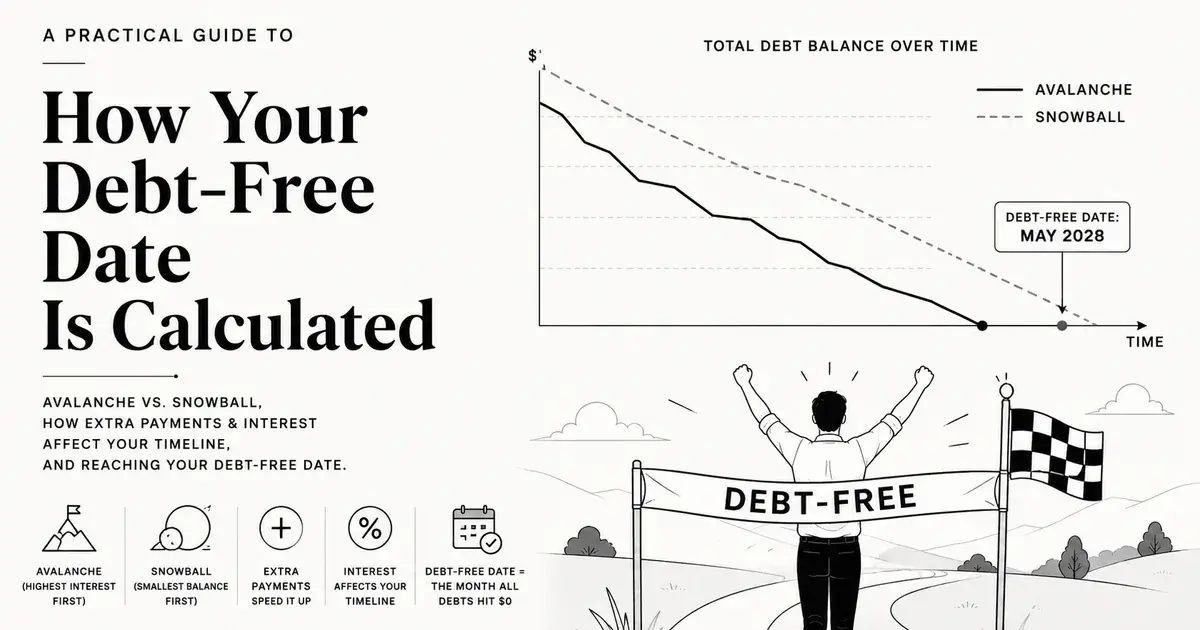

4. Debts (and their payoff)

Mortgages, car loans, student loans, and credit cards each have a balance, an interest rate, and a minimum payment. A good projection shows these balances falling to zero over time and frees up that cash flow for saving once they're gone. (We cover the math of when each debt clears in our debt-free date guide.)

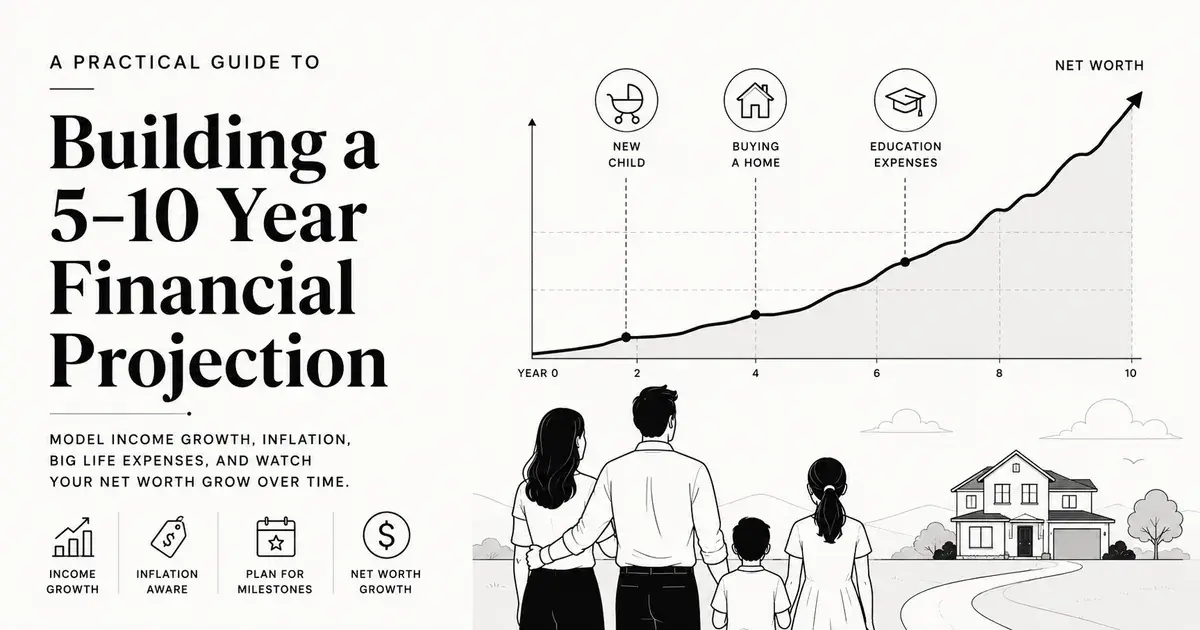

Modeling the big family milestones

Generic projections assume life is smooth. Real family finances have lumps - and those lumps are exactly what you most need to plan for. Build them in explicitly:

- A new child: add childcare as a recurring expense for a defined window (e.g. ages 0–5), plus a one-time bump for the first year.

- A home purchase: model the down payment as a one-time expense in a future month, then add the mortgage as a new debt and property as a new asset from that point forward.

- Education: tuition or a 529 contribution that starts and stops on specific dates.

- Income changes: a planned career break, a return to work, or a partner going part-time - each is just an income source that starts or ends on a date.

The ability to set start and end dates on any income or expense is what makes a projection match a real family's life instead of an idealized average.

Reading the output: cash flow and net worth

A finished projection gives you two views that work together:

- Monthly cash flow - income minus expenses minus debt payments. Positive months build wealth; negative months drain it. Watch for the months a big milestone lands.

- Net worth over time - assets minus debts, plotted across the years. This is the headline number: the line you want trending up and to the right.

Together they answer the real questions. A dip in net worth the year you buy a house is fine if the line recovers and keeps climbing. A cash-flow shortfall during a planned career break is fine if your emergency fund covers it. The projection lets you see the stress test before you live it.

Five mistakes that make projections useless

- Freezing income and expenses. Ignoring growth and inflation makes a ten-year forecast meaningless.

- Forgetting irregular costs. Cars, roofs, and appliances die. Budget for them as periodic one-time expenses.

- Over-optimistic returns. Assuming 10%+ investment growth sets you up for disappointment. Use conservative, long-run averages.

- Treating it as set-and-forget. Revisit your projection once or twice a year and after any major life change.

- Confusing a projection with a guarantee. It's a well-reasoned estimate, not a promise. Its value is in comparing choices, not predicting the future.

Building it in FinProjection

FinProjection was built for exactly this. You add each income source, expense, asset, and debt - with growth rates, inflation, and start/end dates - and it computes a month-by-month, 5–10 year projection of your cash flow and net worth instantly. Debts are paid down automatically using the avalanche strategy, and everything recalculates in real time as you adjust assumptions with what-if sliders.

It's free, requires no signup, and runs entirely in your browser — your financial data never leaves your device. That makes it a safe place to model the most personal numbers your family has.

See your own numbers

FinProjection turns your real income, expenses, debts, and assets into a clear 10-year roadmap - with growth, inflation, and the avalanche debt strategy built in. Free, no signup, 100% in your browser.

Try It Now - It's Free

FinProjection is a planning tool, not financial advice. Projections are estimates based on the assumptions you enter and are not guarantees of future results. Consult a qualified financial professional before making major financial decisions.